A man shows his NHIF card during an activation drive in Meru town on December 6, 2017. About 400 private hospitals will now require patients to pay in cash following a dispute with the NHIF.

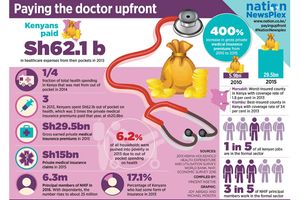

An estimated 400 private hospitals in rural parts of the country will from next Sunday not accept National Health Insurance Fund (NHIF) cards and instead demand that patients pay in cash over an outstanding Sh6.1 billion debt owed by the public insurer.

The Rural Private Hospitals Association of Kenya (Rupha) revealed that NHIF owes them Sh2.3 billion for general claims, Sh2 billion for the Linda Mama programme, and Sh1.8 billion for outpatient claims — a staggering amount that has crippled their operations.

Rupha further claimed that NHIF had not been remitting money to these healthcare facilities. It wasn’t until March that it paid Sh56 million to hospitals that had pending capitation for the January to March quarter.

“Given the foregoing, we have resolved that, instead of continuing to accumulate debts, which we are uncertain will be settled, we transition to a cash-based system and allow the transition to complete then we can resume under new terms,” Rupha chairman Brian Lishenga said.

He said the association’s members had decided to opt out of NHIF until the transition to the Social Health Authority (SHA) is completed. This move means that patients will need to pay for healthcare services in cash, putting the Universal Health Coverage (UHC) initiative in jeopardy.

Dr Lishega said there has been no commitment from either the NHIF or the Ministry of Health to pay the debts.

“These bills have been forwarded to the Pending Bills Verification Committee that is headed by the former auditor-general [Edward Ouko]. Statutory remittances and self-employed contributions to NHIF have been falling since 2022. NHIF collects less every month than it used to do one year ago,” he said.

Rupha has also raised concern over what it termed as biases whenever any money is available, saying, NHIF prioritises payments to levels five and six hospitals first, an approach it opposes.

“With 8,990 hospitals in their database, when will they ever finish?” Dr Lishega posed. The move by the Rupha comes amid uncertainty over the phase out of the long-standing NHIF and replacing it with SHIF. Health Cabinet Secretary Susan Nakhumicha had earlier announced that SHIF deductions would start in March. She then changed this to July before reverting to March, confusing the public even more. The CS further stated that, despite the deductions beginning soon, Kenyans will access services in July.

She explained that the three-month gap will allow the government to prepare adequately to actualise the scheme.

Health Cabinet Secretary Susan Nakhumicha on February 22, 2024.

Dr Lishenga stated that the adoption of the new scheme will depend on the benefits package and contracting terms. The final regulations that will govern the scheme have not yet been published by the Health ministry. Once the regulations are published, an advisory panel will be formed to guide on the benefits package and tariffs.

Responding to the inquiry about when the panel would be formed, Social Health Authority (SHA) chairperson Timothy Olweny said the agency was waiting for the final version of the regulations to be gazetted in order to give a clearer picture.

Under the Social Health Insurance (General) Regulations, 2023, the amount payable each month shall not be less than Sh300 per month. However, for those who are not employed, the amount is paid annually. This means that an unemployed person has to pay at least Sh3,600 every year.

“A household whose income is not derived from salaried employment shall pay an annual contribution to the Social Health Insurance Fund at a rate of 2.75 percent of the proportion of household income as determined by the means testing instrument,” the regulations say.

Rupha has been at odds with NHIF for about two years over the late disbursement of claims.

Last year, Rupha, who represent hospitals in 43 counties, noted that despite numerous assurances from the NHIF Board indicating that payments would be made, their accounts remained empty. As a result, hospitals in rural and urban under-served populations such as Kangemi, Kayole in Nairobi, and Kisauni in Mombasa, resorted to charging NHIF beneficiaries fixed rates under co-pay arrangements for services rendered, where the balance is covered by the insurer.